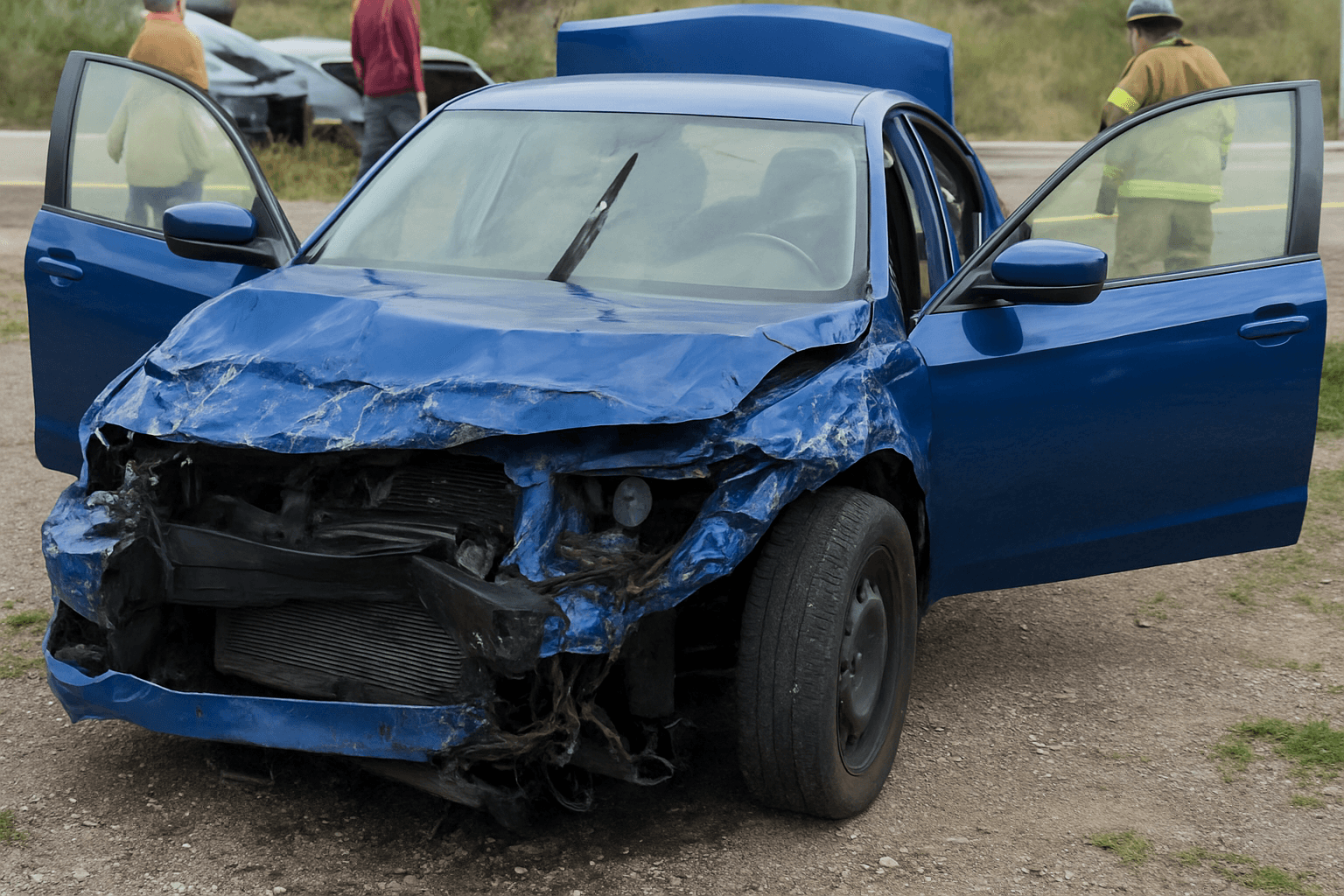

An at-fault accident with bodily injury injury triggers points, a liability claim, and a multi-year surcharge. Here's what to expect on your license and your premium.

Why bodily injury accidents trigger the highest rate increase of any violation

An at-fault accident with bodily injury typically raises your premium 40–70% at renewal, compared to 15–30% for a speeding ticket or 25–45% for an at-fault property-damage-only accident. The difference is claim severity. Bodily injury claims cost carriers an average of $20,000–$65,000 when medical bills, lost wages, and pain-and-suffering damages are tallied, versus $4,000–$8,000 for property damage alone.

Carriers price based on predicted future claim probability. A driver who caused one bodily injury accident is statistically 3–5 times more likely to cause another compared to a driver with a clean record, according to Insurance Information Institute actuarial models. That risk profile translates directly to a surcharge that persists for 3–5 years on most carriers' rating schedules.

The surcharge applies even if your liability limits were adequate and the claim closed without litigation. Carriers don't reward you for carrying higher limits when you cause an accident — they surcharge the accident itself. The only exception: some carriers offer accident forgiveness after 5–7 years claim-free, which waives the first at-fault accident surcharge entirely.

How many points an at-fault bodily injury accident adds to your license

Most states assign 3–4 points for an at-fault accident, regardless of injury severity. California assigns 1 point. North Carolina assigns 3 points. Florida, Georgia, and Texas assign 3–4 points depending on whether a citation was issued at the scene. A few states — including Michigan, Pennsylvania, and Massachusetts — do not use point systems at all, relying instead on conviction counts or carrier-reported accidents to track driver history.

Points stay on your DMV record for 2–3 years in most states, measured from the accident date. Insurance surcharges last 3–5 years, measured from the renewal date when the accident first appeared on your policy. This creates a gap: your DMV record may be clean while your insurance rate is still surcharged. Carriers pull your Motor Vehicle Report at renewal and apply their own lookback window, which is typically longer than the state's point expiry period.

If you're approaching your state's suspension threshold, the bodily injury accident points count the same as speeding ticket points. A driver in North Carolina with 9 existing points who causes a 3-point accident crosses the 12-point suspension threshold. The accident itself doesn't trigger a special suspension category — it's the cumulative total that matters.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

When an at-fault bodily injury accident triggers SR-22 filing

An at-fault accident does not automatically require SR-22 filing in most states. SR-22 is triggered by specific violations: DUI, driving without insurance, repeated license suspensions, or reinstatement after a points-based suspension. If your accident causes a suspension because it pushed you over your state's point threshold, you'll need SR-22 when you reinstate — but the accident itself is not the direct trigger.

The exception: if you caused the accident while uninsured or underinsured, many states require SR-22 as a condition of license reinstatement. Florida, Virginia, and North Carolina require 3 years of SR-22 filing after an uninsured at-fault accident. California requires 3 years if the accident resulted in a judgment you couldn't pay.

SR-22 filing itself costs $15–$50, but the insurance rate for an SR-22 driver with an at-fault bodily injury accident is typically 80–150% higher than standard rates. Most preferred carriers decline SR-22 risks entirely, routing you to non-standard carriers like The General, Safe Auto, or state assigned-risk pools.

How carriers price bodily injury accidents differently than property damage

Carriers assign internal accident severity scores based on claim type and payout. A bodily injury accident scores higher than property damage, and the surcharge reflects that. Progressive, for example, applies a base accident surcharge of 25–35% for property damage and 40–60% for bodily injury, with the exact percentage varying by state and your prior claim history.

Some carriers apply a stepped surcharge model: the first $10,000 of claim payout triggers one surcharge tier, and each additional $10,000 increment escalates the tier. A $5,000 property damage claim and a $50,000 bodily injury claim will not receive the same surcharge, even though both are coded as at-fault accidents on your MVR.

Carriers also distinguish between single-vehicle and multi-vehicle accidents when bodily injury is involved. A single-vehicle accident with passenger injuries may be surcharged less aggressively than a multi-vehicle accident with third-party injuries, because the latter suggests higher third-party liability exposure in future claims. This distinction is internal to the carrier's rating algorithm and does not appear on your DMV record.

What your rate looks like after a bodily injury accident, by point tier

A driver with a clean record who causes one at-fault bodily injury accident can expect a monthly premium increase of $60–$120 in most states, depending on base rate and coverage limits. A driver with one prior speeding ticket who adds a bodily injury accident faces a $90–$150 monthly increase, because the surcharges compound rather than replace each other.

Once you cross into multi-point or multi-violation territory, preferred carriers like State Farm, Allstate, and Nationwide typically decline to renew your policy. You're routed to standard-tier carriers like The Hartford or non-standard carriers like Bristol West, Safe Auto, or The General. Non-standard rates for a driver with 4–6 points and an at-fault bodily injury accident range from $180–$350/mo for state minimum liability, compared to $70–$110/mo for a clean-record driver with the same coverage.

Carriers that specialize in non-standard risks — Dairyland, Bristol West, Acceptance Insurance — price bodily injury accidents less punitively than preferred carriers because their entire book is high-risk. If you're comparing quotes after a bodily injury accident, expect preferred carriers to either decline or quote 70–90% above your prior rate, while non-standard carriers quote 50–70% above clean-record baseline but offer coverage without declination.

How to reduce points or shorten the surcharge window

Most states do not allow point reduction for at-fault accidents, even through defensive driving courses. California, Florida, and Texas permit point masking via state-approved traffic school for moving violations, but accidents are explicitly excluded. New York allows point reduction through the Point and Insurance Reduction Program, but the insurance surcharge persists regardless of DMV point removal.

The only way to shorten the surcharge window is to switch carriers. Some carriers apply a 3-year lookback for accidents, while others apply 5 years. If your current carrier uses a 5-year window and you're 3 years post-accident, shopping your policy to a carrier with a 3-year window can eliminate the surcharge immediately. Non-standard carriers are more likely to use shorter lookback windows because their actuarial models already assume elevated risk.

Accident forgiveness programs, offered by Progressive, Allstate, and Liberty Mutual, waive the first at-fault accident surcharge if you've been claim-free for 5 years prior. These programs are not retroactive — you must enroll before the accident occurs. If you caused a bodily injury accident without accident forgiveness, you cannot add it afterward to erase the surcharge.

When the bodily injury claim stays open longer than the points stay on your record

Bodily injury claims take 6–24 months to close on average, compared to 30–90 days for property damage claims. If the injured party disputes liability, seeks additional medical treatment, or hires an attorney, the claim can remain open for 2–3 years. Your carrier will apply the accident surcharge at the first renewal after the claim is filed, not after the claim closes.

If your claim is still open when your policy renews, some carriers apply a provisional surcharge based on reserves — the estimated payout the carrier has set aside. If the final payout is lower than reserves, the surcharge may decrease at the next renewal. If the payout exceeds reserves, the surcharge increases. This creates rate volatility for drivers with open bodily injury claims.

Once the claim closes, the accident is locked into your claims history database — CLUE (Comprehensive Loss Underwriting Exchange) and A-PLUS (Automobile Property Loss Underwriting Service). These databases are shared across carriers and persist for 7 years, even if your state's MVR only shows the accident for 3 years. When you shop for quotes, every carrier pulls your CLUE report and prices the bodily injury accident based on the closed claim payout, not the DMV point value.