When you get ticketed driving someone else's car, the points go on your license — not theirs. Your insurance sees it the same way they'd see a ticket in your own car.

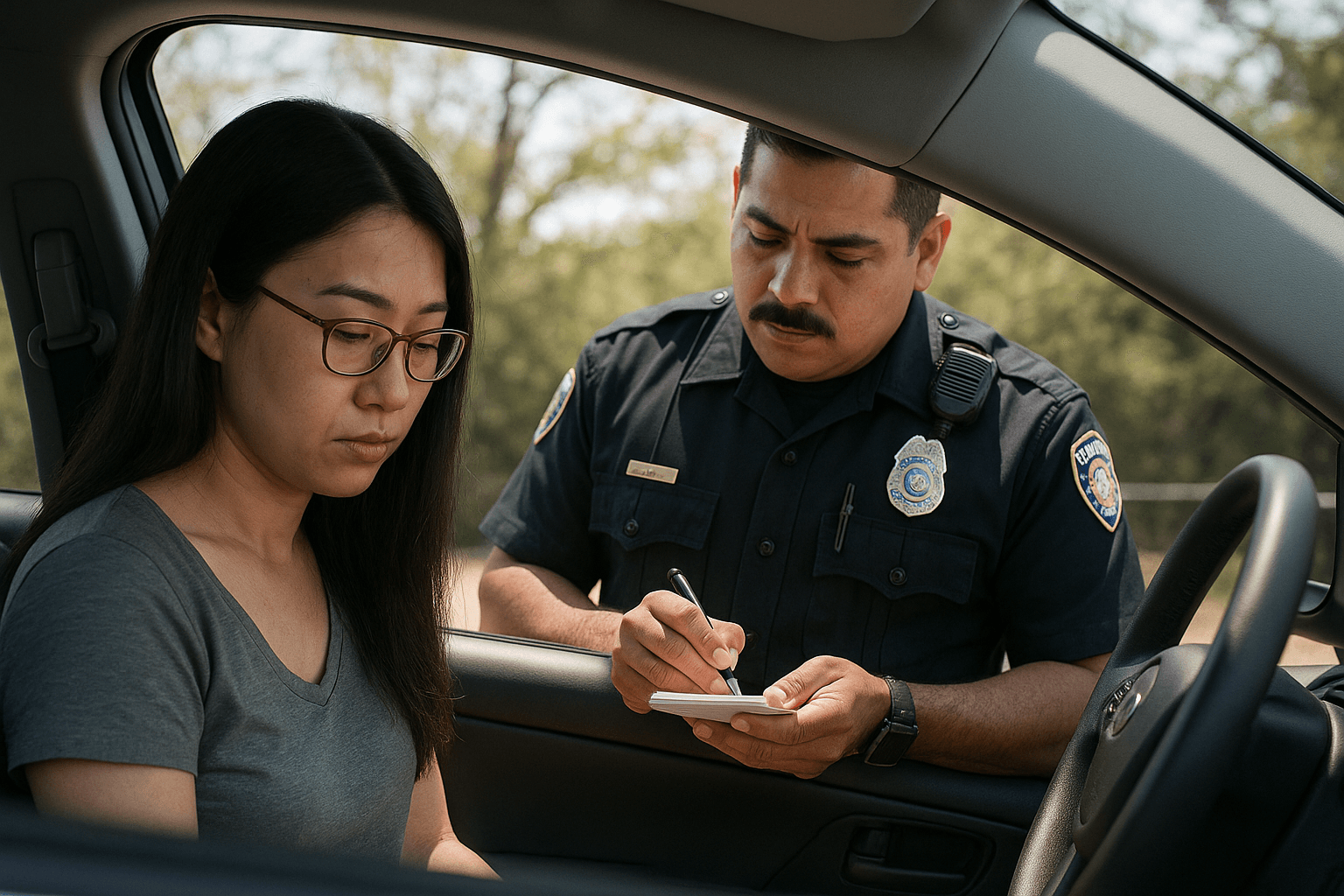

Points Follow the Driver Who Was Cited, Not the Car's Owner

The officer wrote your name on the citation, so the points land on your driving record. State DMVs assign points to the individual driver convicted of the violation, regardless of who owns the vehicle. Your friend's clean record stays clean. Your record now carries the points, the conviction date, and the violation code that your insurance carrier will see at your next renewal.

This holds true even if your friend was in the car, even if they gave you permission, and even if the ticket happened because you were unfamiliar with their vehicle. The citation lists your driver's license number. That's the record the court reports to when you pay the fine or complete traffic school.

Your insurance company pulls your motor vehicle report during underwriting. They see every moving violation tied to your license, whether you were driving your own car, a borrowed car, a rental, or a company vehicle. The vehicle identification number doesn't determine surcharge eligibility — your driver's license does.

Your Insurance Rate Increases, Not Your Friend's

Your carrier applies the surcharge to your policy at renewal because the violation appears on your MVR. A single speeding ticket typically triggers a 15-30% rate increase that lasts three years on most surcharge schedules. If you carry your own policy, expect the increase when your term renews. If you're listed as an occasional driver on a parent's or spouse's policy, the household policy absorbs the surcharge — but it's still your violation causing it.

Your friend's insurance sees nothing. Their carrier has no reason to pull your driving record, and the ticket doesn't appear on their MVR. Even if you were driving their car when cited, their policy rates stay unchanged unless they've listed you as a regular driver on their policy — and most lenders of cars for a single trip have not.

Carriers distinguish between the insured driver and the occasional permissive user. Your friend extended permissive use when they handed you the keys. Their liability coverage applied at the moment of the ticket if you'd caused an accident, but permissive use doesn't transfer citation liability. The ticket stays yours, and so does the financial consequence.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

How Long the Violation Affects Your Driving Record and Insurance

Points stay on your DMV record for a state-specific window, often three years from the conviction date. Your insurance surcharge typically lasts three years as well, but the two timelines don't always align. Some states remove points after 18 months while carriers continue the surcharge for the full 36-month lookback period.

Most carriers review your MVR at every renewal. If the violation occurred 20 months ago and your state removes points at 24 months, you'll still pay the surcharge for one more annual term because the conviction itself remains visible even after points drop off. Carriers rate on convictions, not point totals — the points are a DMV licensing tool, not an insurance pricing input.

Once the violation ages past your carrier's lookback window, the surcharge ends automatically at the following renewal. You don't need to request removal or file paperwork. The conviction date controls the timeline, and that date is the day the court processed your payment or guilt plea — not the day you were pulled over.

Whether Defensive Driving Removes Points from This Violation

Many states allow drivers to complete a defensive driving course to remove points from a recent violation, but eligibility rules vary. Some states let you take the course once per 12 or 24 months. Others restrict it to first offenses or violations under a certain speed threshold. If your state permits point reduction and the violation qualifies, completing the course removes the points from your DMV record.

Removing points from the DMV does not automatically remove the insurance surcharge. Your carrier still sees the original conviction on your MVR — the course just prevents the points from pushing you closer to a license suspension. You'll need to ask your insurer whether they offer a discount for course completion. Some do. Many don't, and the surcharge continues for the full lookback period even with zero points on your license.

Check your state DMV's point reduction eligibility before enrolling. Courts sometimes require you to request permission before completing the course, and deadlines are strict. Missing the window means you pay for the course but gain no DMV benefit. If the course is approved and completed on time, request a copy of your updated MVR and send it to your insurer with a written request for re-rating.

What Happens If You Don't Carry Your Own Insurance Policy

If you don't own a car and don't carry your own policy, the violation still appears on your MVR and affects you when you do buy coverage. Carriers pull your driving history during the quote process. A speeding ticket from two years ago, even if you weren't insured at the time, will be priced into your first premium.

Non-owner car insurance policies exist for drivers who borrow cars frequently but don't own a vehicle. These policies provide liability coverage when you drive someone else's car and act as continuous coverage to avoid a lapse penalty. If you were on a non-owner policy when the ticket happened, that policy will surcharge at renewal just like a standard auto policy.

Drivers without any policy at the time of the violation face a worse situation when they later buy coverage. Carriers treat the combination of a violation and a coverage lapse as high-risk. The ticket alone might add 20%. The lapse might add another 30-50%. Together, they can double your base rate compared to a clean-record driver with continuous coverage. Buying a non-owner policy immediately after the ticket, even if you don't drive often, preserves continuous coverage and limits the total rate impact when you eventually need a standard policy.